Profits Before Principles: How AARP Wins When Seniors Lose

A report originally compiled by staff for Sen. Jim DeMint.

REPORT HIGHLIGHTS

- AARP functions as an insurance conglomerate with a liberal lobbying arm on the side. Independent experts and former AARP executives admit that the organization’s billions of dollars raised from its business enterprises – most notably the sale of health insurance plans – have compromised the organization’s mission and independence.

- AARP depends on profits, royalties, and commissions to make up over 50% of its annual budget. Membership dues from seniors account for only about 20% of AARP’s revenue.

- AARP’s $458 million in health insurance revenue in 2011 would rank it as the nation’s sixth-most profitable health insurer.

- The health care law, which AARP lobbied heavily for, could lead to over $1 billion in new AARP health insurance profits over the next decade by forcing seniors off Medicare Advantage plans into Medigap supplemental coverage.

- AARP earns more profit the higher premiums rise on seniors in Medigap plans, charging a “royalty fee” of 4.95% of every premium dollar paid by seniors on these plans.

- In 2011, AARP failed to disclose to its senior membership that it lobbied Congress to oppose Medigap reform, legislation that could lower senior premiums by as much as 60%, and save seniors $415 per year on average.

- AARP could lose as much as $1.8 billion in revenue over ten years if Medigap reforms pass and successfully lower senior premiums.

- Documents show close coordination between Obama Administration and AARP, including efforts to deceive the public. In November 2009, a senior AARP executive wrote to the White House saying “we will try to keep a little space between us” on health care – because AARP’s “polling shows we are more influential when we are seen as independent, so we want to reinforce that positioning….The larger issue is how best to serve the cause.”

- AARP has benefitted by supporting the Obama Administration’s unpopular health care law. Unlike other forms of insurance, AARP’s Medigap insurance plans were exempted from many of the health care law’s mandates, including the ban on pre-existing condition discrimination.

- The Obama Administration has not publicly criticized AARP’s business practices, even though it has publicly attacked other insurance companies with much smaller profit margins than those generated by AARP’s Medigap insurance.

- Democrats continue to praise AARP – HHS Secretary Sebelius called them the “gold standard” for “accurate information” – even though AARP earns more profit the higher Medigap premiums rise for seniors.

Even though President Obama has criticized Republicans for placing seniors at the mercy of insurance companies, the health care law he signed allows organizations like AARP to continue discriminating against Medigap applicants with pre-existing conditions.

Introduction

The AARP bills itself as the nation’s premier senior advocacy group, but has opposed important reforms to Medigap supplemental insurance that would save seniors, on average, hundreds of dollars a year.

Why? There are $1.8 billion reasons.

The reforms currently being proposed to Medigap would drastically reduce the “royalty fees” AARP generates by peddling insurance to its members by an estimated $1.8 billion over ten years. If AARP supported these reforms, which are sure to save seniors money, the lobbying group would lose billions.

This report shows how the AARP has a history of being compromised by its lucrative insurance businesses. The pressure group’s opposition to Medigap reform is just the latest instance where its financial enterprises have trumped the well-being of its members.

AARP is mounting a “You’ve Earned a Say” campaign to solicit member viewpoints about how to reform entitlements, but our examination of the organization’s actions over the years shows AARP executives, who seek to boost their bottom lines, always have the biggest say.

The AARP Empire

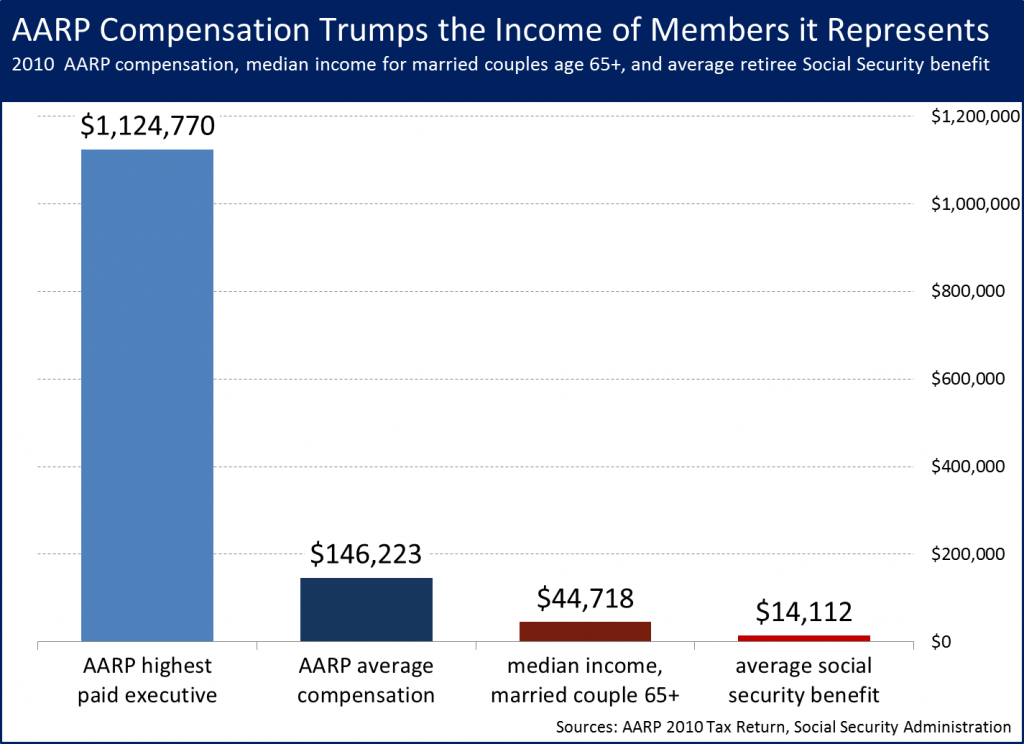

Founded in 1958, AARP is now an organization with an annual budget exceeding $1 billion. The organization spent $206 million to acquire its headquarters building in Washington, DC more than a decade ago.[1] According to its most recently filed tax returns, AARP spent more than $246 million on postage, and over $280 million on compensation in 2010.[2] In that same year, AARP provided compensation of over $100,000 to 543 separate employees, including one senior executive who received nearly $1.2 million in compensation.[3]

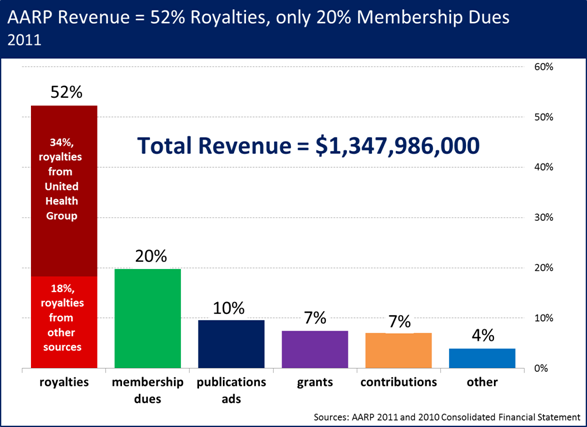

While AARP claims to be a membership-driven organization, in reality most of its revenue comes not from member dues but from “royalty fees” generated from the sale of other products, namely health insurance. “Royalty fees” are payments AARP receives for putting its brand name on certain products and services. So while insurance companies provide a tangible product and service in exchange for the premiums they charge, AARP receives more than half a billion dollars per year for essentially playing the middle man.

According to its 2011 financial statements, more than half of AARP’s revenue came from royalty fees – over $704 million of its $1.35 billion in total revenue last year.[4] Revenues from health insurer United Health Group comprised nearly two-thirds of AARP’s total “royalty fee” revenue, or $457.6 million.[5] By comparison, in 2011 AARP generated only $265.8 million from membership dues – just over half the amount received from the sale of AARP-branded insurance products.[6]

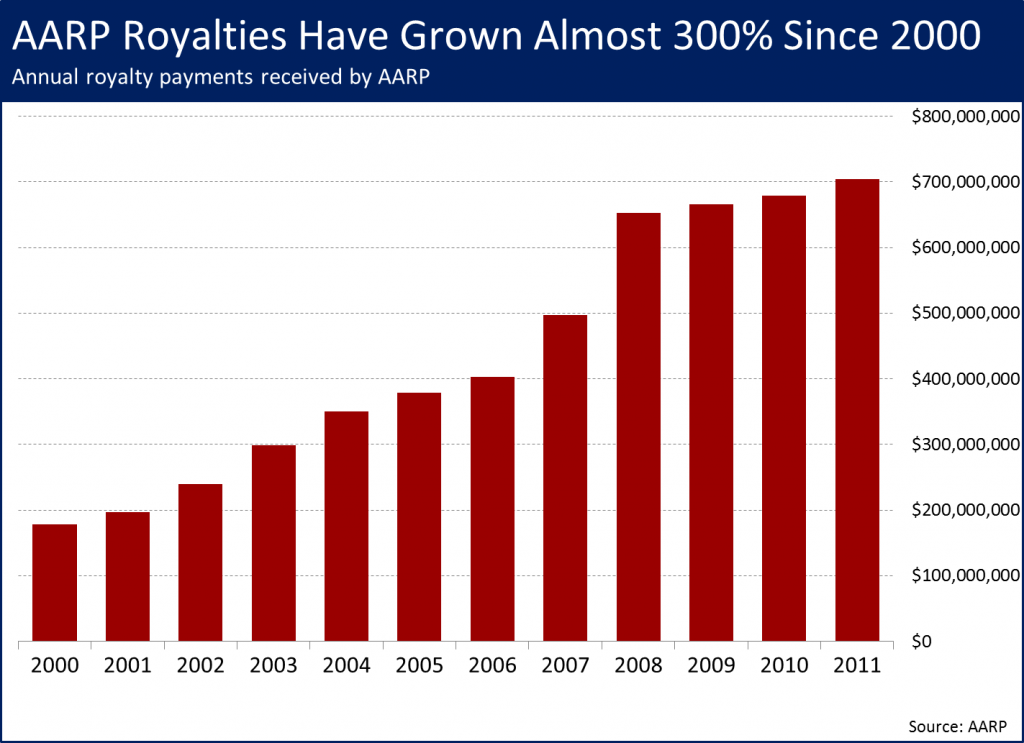

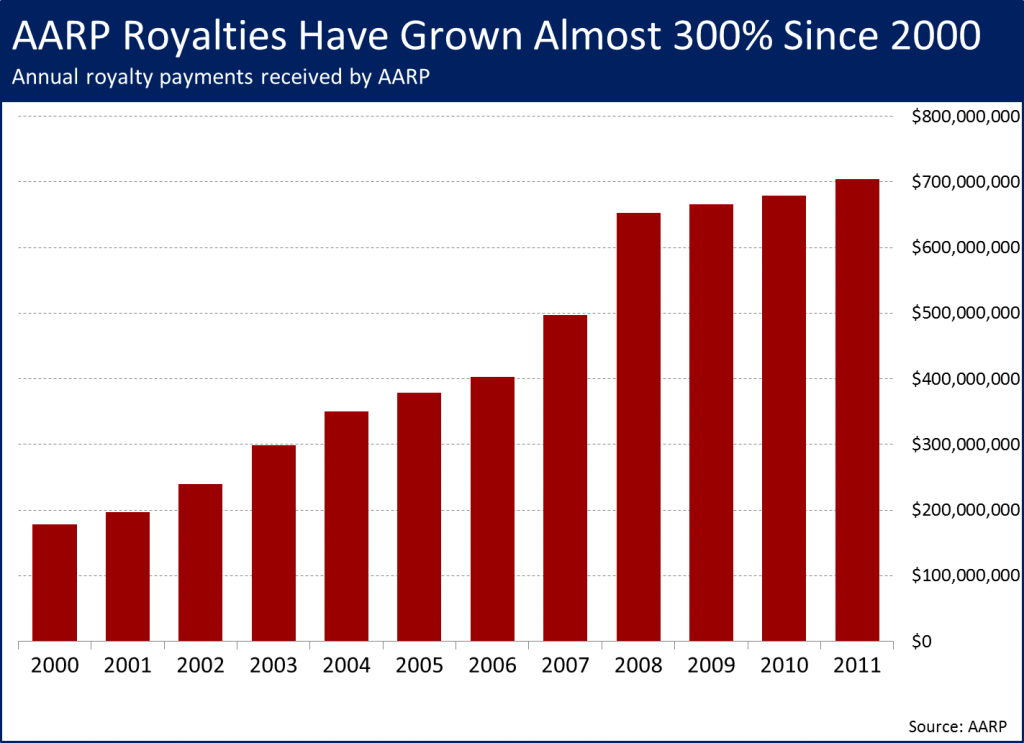

AARP’s royalty fees have risen significantly in recent years, making the organization ever more dependent on the sale of insurance policies to fund AARP’s massive payroll. Between 2001 and 2011, AARP’s total royalty fees rose by more than 350% – from $196.7 million in 2001 to over $704 million last year.[7] Much of this increase comes from additional health insurance-related revenue. Over the past five years, AARP has generated over $2 billion in revenue from United Health Group alone – $284 million in 2007,[8] $414 million in 2008,[9] $427 million in 2009,[10] $441 million in 2010,[11] and $458 million in 2011.[12]

AARP’s $458 million in insurance revenue in 2011 would rank it as the nation’s sixth-most profitable insurer, based on data collected by Fortune magazine.[13] For instance, insurer Health Net generated only $204 million in net revenue last year – on over $13.6 billion in total revenue.[14] By contrast, AARP’s $458 million in insurance-based “royalty fees” go directly to the organization’s bottom line.

AARP’s Questionable Insurance Practices

Even as it claims to be a non-profit advocacy organization, AARP has received criticism from many quarters for its heavy reliance on revenue from insurance sales. Marilyn Moon, a former AARP executive, said “there’s an inherent conflict of interest” because AARP is “very dependent on sources of income.”[15]

AARP’s dependence on “royalty fee” income has resulted in numerous controversies over the years. For instance, in 2008 a congressional inquiry[16] found that AARP was using potentially misleading language in its marketing materials; seniors thought they were buying comprehensive health insurance, but in reality purchased policies covering only a limited amount of health costs. Following a public outcry, AARP ordered an investigation,[17] and eventually stopped selling these types of limited benefit plans.[18]

More recently, the tax implications of AARP’s significant “royalty fees” have come under scrutiny. An investigation by several members of the House Ways and Means Committee last year raised questions about whether or not AARP’s licensing revenue should be considered “royalty fees” or “commissions.”[19] If the revenue in question should in fact be classified as “commissions,” then AARP could owe significant amounts of back taxes on billions of dollars in revenue. The Ways and Means members referred the matter to the Internal Revenue Service, and requested an IRS investigation.[20]

The Medigap Cash Cow

The Ways and Means member investigation also made clear that one of AARP’s prime sources of revenue is the sale of Medigap-branded supplemental insurance plans. AARP does license Medicare Advantage plans, along with a Medicare Part D prescription drug plan. However, AARP receives a flat financial payment from United Health Group for its Medicare Advantage and Part D plans, regardless of the number of people enrolled in each plan. Conversely, AARP receives a percentage of total Medigap premiums paid – meaning that while AARP receives no financial benefits if its Medicare Advantage or Part D plan enrollment rises, it will receive a windfall if its Medigap plan generates additional customers, or those customers pay higher premiums.

The health care law includes more than $300 billion in cuts to Medicare Advantage.[21] As a result of these payment reductions, enrollment in Medicare Advantage plans will be cut in half, with 7.4 million fewer seniors enrolled.[22] Many of these 7.4 million seniors will need supplemental coverage through Medigap, to fund catastrophic expenses not covered by Medicare.

Because the health care law will have the effect of migrating millions of seniors from Medicare Advantage plans – which are less lucrative financially to AARP – to more-lucrative Medigap supplemental coverage, the Ways and Means member report concluded that the organization could receive a windfall exceeding $1 billion over the next ten years thanks to the law.[23]

Medigap Reform with Bipartisan Appeal

The potential Medigap-related windfall for AARP resulting from the health care law is not the only instance in which the organization’s financial interests have coincided with its policy positions. In recent months, a renewed focus on reforming entitlements, and making Medicare more sustainable, has prompted new attention to various proposals to reform Medigap plans. While these plans would benefit most seniors financially, they would harm AARP’s financial interests – so perhaps not surprisingly, AARP has decided to oppose them.

Under the proposals being discussed, the traditional Medicare program would be reformed to provide catastrophic coverage, while Medigap would provide limited supplemental coverage. For the first time in the program’s history, seniors would know their Medicare costs would not exceed a set amount. In exchange, Medigap supplemental coverage, which covers co-payments and deductibles, would also be reformed, so that seniors would face an out-of-pocket deductible not covered by insurance.

Reform to Medigap insurance plans has generated bipartisan appeal. Versions of this reform have been proposed by the Simpson-Bowles Commission,[24] the Rivlin-Domenici commission on debt and deficits, [25] Sens. Tom Coburn (R-OK) and Joe Lieberman (D-CT),[26] and even President Obama’s most recent budget.[27] Policy-makers in both parties believe that, by limiting first-dollar coverage of medical expenses through Medigap, seniors would serve as smarter purchasers of health insurance, such that overall spending in Medicare might decline modestly.

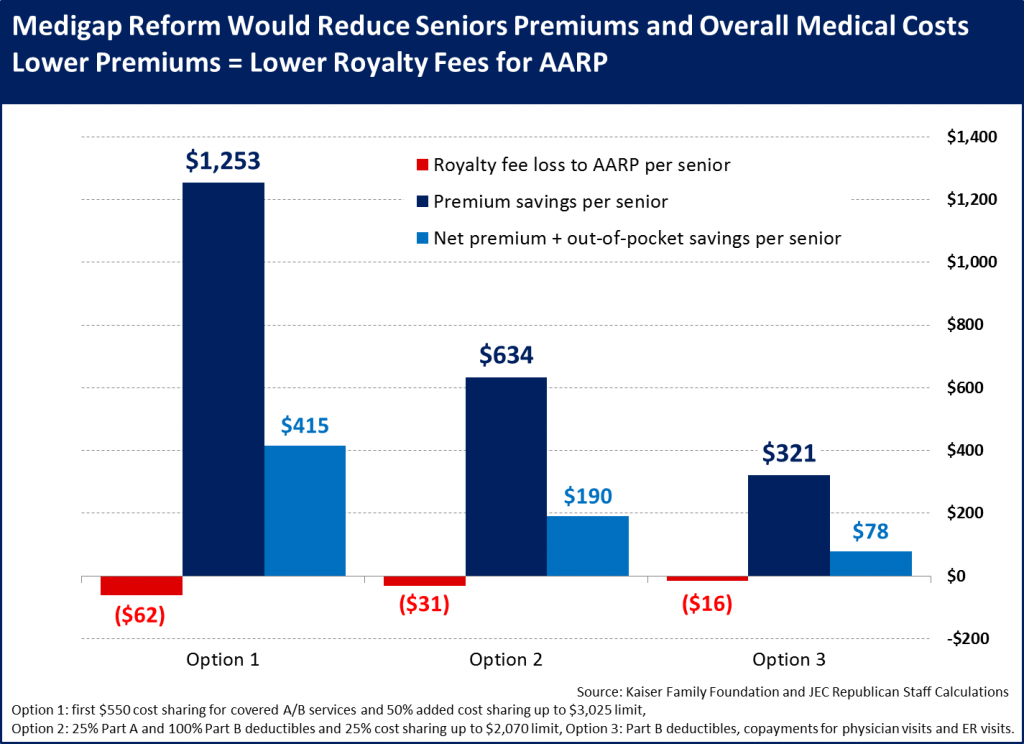

Although some seniors might pay slightly more out-of-pocket under these changes, a study from the Kaiser Family Foundation said that “the savings for the average beneficiary” under Medigap reform “would be sufficient to more than offset his or her new direct outlays for Medicare cost sharing.”[28] According to Kaiser, nearly four in five Medigap policy-holders would receive a net financial benefit from this reform – with those savings averaging $415 per senior each year – because creating a new deductible for all Medigap plans will cause premiums to fall.[29]

Under Medigap reform, seniors would spend much less money on premiums. Just as with automobile insurance, or with Health Savings Account policies for individuals under age 65, adopting a higher deductible would yield significant premium savings for Medigap policies. The Kaiser study found that under one proposed reform, Medigap premiums would plummet by an average of over 60%, from nearly $2,000 per year to only $731.[30] Because less money from Medigap policy-holders would be diverted to administrative overhead, seniors would be able to keep their own money to finance their own health care.

AARP Wins When Seniors Lose

The overall premise of Medigap reform is simple: Less money going to insurance companies means greater financial savings for most seniors.

Unfortunately for AARP, things are not that simple. As one independent financial adviser has said, AARP’s sales tactics are a “dirty little secret” that are “all about fattening the coffers of the organization.” And the biggest “dirty little secret” of all is that AARP has a major financial incentive to keep premiums high for seniors.[31]

The House Ways and Means Committee members’ investigation last year found that AARP receives a percentage of each senior’s Medigap premium dollar.[32] The organization’s “royalty fee” totals 4.95% of every premium dollar paid. So, similar to a salesman pushing the most expensive product in order to receive a higher commission, regardless of the customer’s needs, AARP has an incentive to sell more Medigap policies – and to sell the most expensive Medigap policies – even if seniors do not need the insurance. The higher the cost of seniors’ Medigap policies, the more money AARP makes.

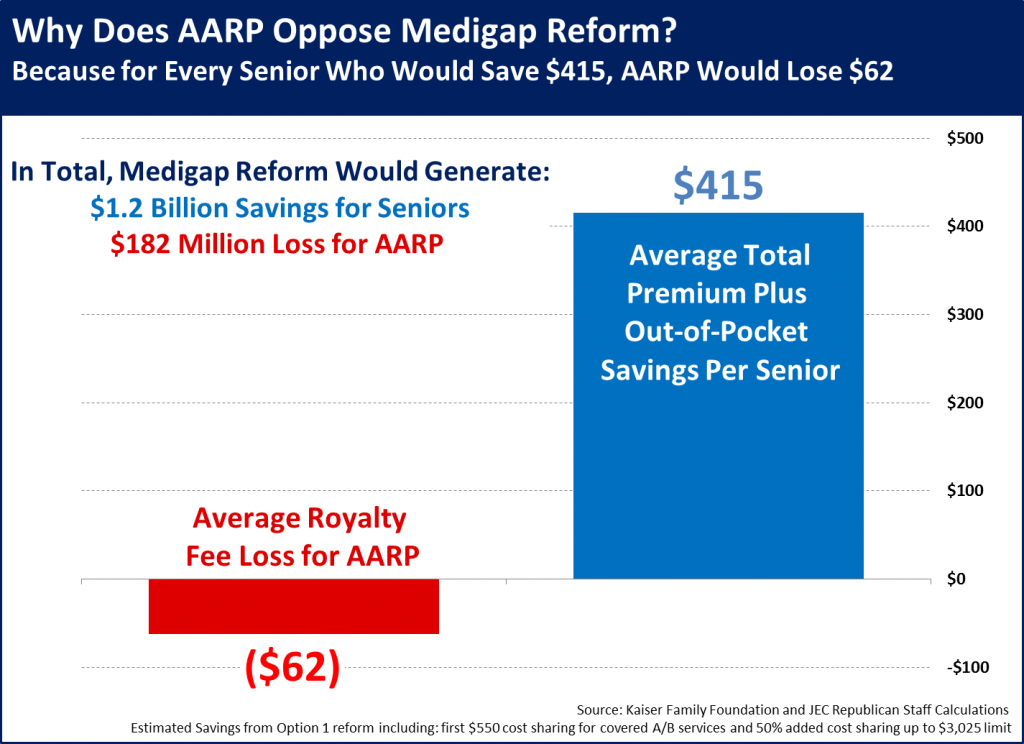

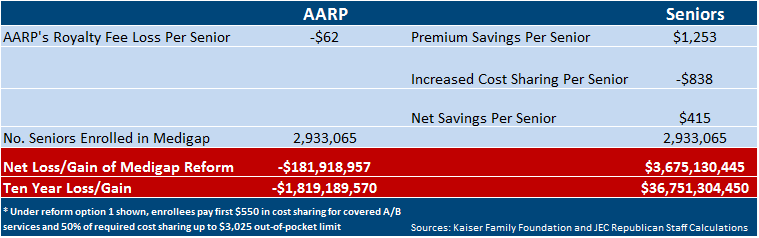

Based on AARP’s existing contractual arrangements and the Kaiser Family Foundation study projections, it is relatively simple to calculate the projected financial loss to AARP under Medigap reform.[33] If premiums decline by more than $1,200 per year, as the Kaiser study predicted, AARP stands to lose an average of $62 in “royalty fees” for every senior enrolled in its Medigap insurance. With nearly 3 million seniors enrolled in AARP’s Medigap plan, those numbers add up – over $181 million in one year, and $1.8 billion over the course of a decade.[34] With the organization generating total revenue of $1.35 billion in 2011, Medigap reform would result in an immediate loss of over 13% of AARP’s annual revenue.[35]

AARP’s Covert Campaign to Kill Medigap Reform

Given its financial interest in keeping Medigap premiums high, it is perhaps unsurprising that AARP engaged in a covert lobbying campaign designed to kill Medigap reform, and keep its existing “royalty fee” regime in place. Last year AARP wrote to members of the congressional “supercommittee” on deficit reduction, asking them not to include Medigap reforms – which, as noted above, would benefit four out of five Medigap policy-holders, but significantly harm AARP’s financial interests.

AARP published excerpts of their letter to the “supercommittee” on its website.[36] But AARP has yet to put anything on its website indicating that the organization has been privately contacting Members of Congress, asking them not to reform Medigap – and preserve AARP’s lucrative Medigap commissions.

Two years ago, an AARP spokesman told CNN that the organization doesn’t lobby Congress on Medigap issues “at all.”[37] While the organization is apparently trying to keep its actions secret, the fact remains that AARP is lobbying Congress against Medigap reform, opposing changes that will just so happen to save AARP members tens of billions, but that would also cost AARP billions.

AARP Works Against Its Members

Whereas last year AARP actively lobbied against Medigap reforms that would help its members but hurt AARP financially, three years ago the organization did NOT lobby for Medigap reforms that would help its members but could hurt AARP financially. Specifically, even after enactment of the health care law, Medigap plans are still permitted to impose waiting periods on senior citizen applicants with pre-existing conditions. AARP, despite its stated support for ending pre-existing condition restrictions,[38] imposes waiting periods on its own members applying for Medigap coverage[39] – and stood idly by as an attempt to end this practice within Medigap was stricken from the health care bill before it became law.

Section 1234 of House Democrats’ June 2009 health care discussion draft would have prohibited pre-existing condition discrimination for certain Medigap applicants – achieving one of AARP’s chief goals.[40] However, last year the Washington Post claimed that the Medigap provision “was dropped from the legislation during congressional negotiations because it would have increased Medicare costs, according to a House Democratic congressional aide.”[41]

The Congressional Budget Office scored provisions eliminating pre-existing condition discrimination in Medigap as costing about $400 million per year.[42] However, AARP had previously stated that the organization “would gladly forego every dime of revenue to fix the health care system.”[43] As noted above, its $700 million in “royalty fees” last year far exceeds the $400 million annual cost of ending Medigap pre-existing condition discrimination. It remains unclear why this provision was dropped from the bill, if AARP was so interested in foregoing profits in order to help its members.

In addition to allowing AARP to continue imposing waiting periods on Medigap applicants, the law enacted in March 2010 also exempted AARP’s lucrative Medigap policies from several other new insurance regulations.[44] At a December 2009 hearing,[45] AARP’s Board Chair claimed to have no idea that legislation that she and the AARP had previously endorsed included numerous exemptions for Medigap plans, including an exemption from the ban on pre-existing condition discrimination.[46]

After the numerous Medigap-related exemptions included in the health care law were publicly exposed, AARP eventually endorsed legislative changes to end some of the exemptions.[47] However, despite this public turn-around, AARP has yet to explain to the public why it allowed these exemptions to be enacted in the first place – if the organization is not motivated by its own financial interests, as it claims. Moreover, the organization has not apologized to its members for failing to act and end pre-existing condition discrimination in Medigap plans two years ago, and the impact such failure has had on AARP’s own members.

Members REVOLT

Documents released by a House Energy and Commerce Committee oversight investigation reveal just how strongly AARP members opposed their organization’s behavior during the health care debate three years ago. The files show overwhelming opposition from AARP members to the legislation, based on summaries of AARP call center activity:

July 23, 2009 – 77 members support; 1,031 oppose

July 28, 2009 – 36 members support; 4,174 oppose

July 29, 2009 – 23 members support; 2,656 oppose[48]

On a single day (July 28, 2009) during the height of the debate, 1,897 individuals cancelled their membership in AARP to protest its position on the health care bill.[49]

The documents also reveal that AARP members were well aware of the organization’s financial conflicts, and believed that these conflicts were influencing AARP policy. One member from Oklahoma called in and complained that:

AARP has a conflict of interest between selling insurance and helping senior citizens. Until it decides which one is more important, the $$$ or the people, it is deceiving old folks into thinking it works for their benefit. Actually it works for the insurance companies [sic] benefit and interests, which is why it is so gung-ho on the health care reform bill….Not OK with me.[50]

Members also complained about “perceived partisanship on AARP’s part” – and the documents reveal this to be an accurate concern. In November 2009, a senior AARP executive wrote to the White House saying “we will try to keep a little space between us” on health care – because AARP’s “polling shows we are more influential when we are seen as independent, so we want to reinforce that positioning….The larger issue is how best to serve the cause.”[51] In other words, the organization was attempting to protect its image by publicly deceiving its members – acting detached in public, even as AARP was frantically lobbying behind the scenes to ram the legislation through for the good of the liberal cause.

AARP’s Misguided Political Focus

It is perhaps unsurprising that AARP would focus on “serv[ing] the cause” of liberalism, because many of its senior executives have strong liberal connections. When the organization hired its current CEO, Barry Rand, one Capitol Hill publication noted that “New AARP Chief Gave Big to Obama.”[52] Indeed, Mr. Rand has given tens of thousands of dollars in contributions to liberal Democrats over the years.[53] Many other members of AARP’s executive team also have strong connections to liberal causes; the head of AARP’s government relations and advocacy program was a senior adviser in the Clinton Administration,[54] while other AARP key executives have worked for Sen. Ted Kennedy,[55] Rep. Geraldine Ferraro,[56] and the National Wildlife Federation, a liberal environmental group.[57]

The political philosophy of the organization’s leadership results in AARP mounting advocacy campaigns trumpeting liberal talking points that frequently have little basis in fact. For instance, in September 2011 AARP released an advertisement with seniors claiming that “I paid into my Medicare,” and decrying any efforts to “cut our benefits.”[58] However, the ad did not acknowledge what an Urban Institute study makes clear: Most seniors receive more in Social Security and Medicare benefits than they paid in taxes during their lifetime.[59] An Associated Press story based on the Urban Institute study – “What You Pay for Medicare Won’t Cover Your Costs” – was initially placed on aarp.org, but was later removed from the website, perhaps because its conclusions represent inconvenient truths to AARP.[60]

Other ads run by the AARP during last year’s debt limit debate were also debunked as false and misleading. In June 2011, the Washington Post’s “Fact Checker” column awarded an AARP ad four “Pinocchios” for “perpetuat[ing] the worse stereotypes about how easy it would be to balance the budget. At a time when the nation’s fiscal crisis – amid the looming retirement of the baby-boom generation – demands informed and reasoned debate, the AARP misinforms its members about the choices the nation faces.”[61]

Of course, AARP has a financial interest in misinforming its members – because the organization derives much of its revenue from preserving the status quo. In launching a “multi-million dollar” ad campaign featuring misleading claims, AARP made clear it wanted no changes to the existing Medicare benefit structure.[62] As outlined above, changes to the Medicare benefit – such as Medigap reform – would cost AARP billions, while saving many seniors hundreds of dollars per year. By blocking reforms that would dent its profits, AARP hurts seniors two ways – first, by preventing seniors from saving hundreds of dollars in Medigap premiums, and second, by leaving the Medicare program less solvent for future generations.

Democrats Encourage AARP’s Abuses

Even as AARP racks up billions of dollars in insurance profits by overcharging seniors for Medigap plans, Democrats encourage these abuses by giving AARP special favors, and ignoring its questionable sales tactics. As noted above, the health care law exempted AARP’s lucrative Medigap insurance plans from the ban on pre-existing condition discrimination, thus allowing AARP to continue to impose waiting periods on individuals applying for coverage. However, that’s not the only exemption that Medigap coverage received in the law; Medigap insurance was also exempted from:

- The law’s $500,000 cap on executive compensation for insurance industry executives. [63] Thanks to this exemption, AARP can continue to pay its senior executives more than $1 million in annual compensation.[64]

- The tax on insurance companies that will total more than $14 billion per year.[65] Medigap insurance received this exemption even though AARP generates more money from insurance industry “royalty fees” than it received from membership dues, grant revenues, and private contributions combined.[66]

- The requirement imposed on other health insurance plans to spend at least 85 percent of their premium dollars on medical claims.[67] Medigap policies are currently held to a far less restrictive 65 percent standard, and the difference can be used to fund higher profits to AARP paid out of the pockets of its senior citizen members.[68]

In addition to these numerous exemptions for Medigap insurance provided in law, the Administration provided a further exemption for Medigap coverage during the rulemaking process. The Department of Health and Human Services’ rule on insurance rate review exempted Medigap plans from further scrutiny of their premium increases.[69] In arriving at this determination, HHS concluded that insurance plans like Medigap coverage “do not appear to be a principal focus of the Affordable Care Act” – meaning that because Medigap plans were exempted from the law’s other regulatory requirements, they should be exempted from rate review as well.[70]

Obama Administration Hypocrisy

The frequent exemptions given to Medigap insurance – a product line where AARP holds the largest market share – directly contradict the claims made by Democrats about the 2,700 page health care law. For instance, Department of Health and Human Services Secretary Kathleen Sebelius’ official biography claims that she “is implementing reforms that end many of the insurance industry’s worst abuses.”[71] However, with respect to Medigap insurance, that claim is entirely false. Because Medigap plans were exempted from the law’s new requirements, organizations like AARP can continue to discriminate against applicants with pre-existing conditions, and overcharge seniors in order to generate greater profits.

Even as the Obama Administration fails to acknowledge that the health care law exempts Medigap insurance from all of its new requirements, it has attacked conservatives’ Medicare reform proposals for granting too much power to insurers. In her speech to the 2012 Democratic National Convention, Secretary Sebelius criticized Republicans for “let[ting] insurance companies continue to cherry-pick who gets coverage and who gets left out, priced out, or locked out of the market.”[72] And in his speech to the same convention, President Obama said that “no American should have to spend their golden years at the mercy of insurance companies.”[73] Given that the legislation President Obama signed into law exempted Medigap coverage for seniors from virtually all of its new regulatory requirements, it is more than a little hypocritical for his Administration to criticize others for leaving seniors to the mercy of insurers.

The Administration has yet to answer a basic question at the heart of the numerous exemptions granted to Medigap insurers in their 2,700 page health care law: If the law’s protections are so good, then why are seniors left out of its supposed benefits when it comes to their supplemental insurance? Unfortunately, the answer could be that AARP has been unwilling to forfeit its profits, and so the Obama Administration has looked the other way as the organization continues to take advantage of seniors.

Kathleen Sebelius: Watchdog or Lapdog?

Even as it has been willing to politically strong-arm insurance companies with whom it disagrees, the Obama Administration’s Department of Health and Human Services has failed to confront AARP about its questionable business practices. In March 2010, as the Administration was gearing up to ram through its health care law, Secretary Sebelius asked other insurers to “give up some short-term profits” for the nation’s good.[74] At the time, estimates by Fortune magazine indicated that health insurer profits averaged about 2.2 percent.[75] Yet Secretary Sebelius made no such request of AARP to give up some of its revenues – even though its Medigap profit margin was 4.95 percent, more than double that of the insurance industry as a whole.

Shortly after the health law passed, Secretary Sebelius undertook a publicity campaign to “encourage” insurance companies to ban rescissions and extend coverage to young adults under age 26 earlier than was required under the law. While the Secretary made very public efforts to have insurance companies “abandon…efforts to rescind health insurance coverage from patients who need it most,” she made no attempt to encourage AARP and other Medigap insurers to stop discriminating against applicants with pre-existing conditions.[76] At an implementation briefing to Congress shortly after the law passed, Senate Republican staff asked HHS officials why the Department was asking other insurers voluntarily to change their business practices, but was not asking AARP to stop discriminating against Medigap applicants. While Jeanne Lambrew, head of the Department’s Office of Health Reform, promised to look into the matter, the Department never took action.

Rather than ask AARP to reform its business practices, Secretary Sebelius instead has blindly offered the organization praise. In an October 2010 speech to the AARP convention, she hailed the organization as “the gold standard in cutting through spin and complexity to give people the accurate information they need to make the best choices.”[77] Even though AARP has a strong financial conflict-of-interest in its Medigap insurance – because the organization earns more profit when seniors pay more in premiums – Secretary Sebelius still claimed that AARP constituted “the gold standard” in giving “accurate information.”

The National Association of Insurance Commissioners (NAIC) has previously expressed strong concerns about the percentage-based compensation model under which AARP receives much of its revenue. In fact, Section 18 of NAIC’s Producer Model Licensing Act recommends that states require explicit disclosure by insurers, and clear written acknowledgement by consumers, of any percentage-based compensation arrangement, due to the potential for abuse. As a former insurance commissioner, Secretary Sebelius should be well aware of the financial conflicts inherent when an organization like AARP receives a percentage of every Medigap dollar paid by seniors. Yet the Secretary apparently ignored these concerns, and went on to praise AARP as a source of impartial advice, even though even former AARP executives have criticized the organization as hopelessly compromised by financial conflicts-of-interest.

In her time heading HHS, Secretary Sebelius has undertaken clearly political actions, including those that violated the law. Just last week, the Office of the Special Counsel publicly released a report concluding that the Secretary engaged in political activity that violated the Hatch Act prohibitions on federal officials campaigning for partisan political causes.[78] It is therefore quite reasonable to ask whether Secretary Sebelius has also engaged in a pattern of politically-motivated selective enforcement – attacking other insurers when convenient, but failing to examine AARP’s questionable business practices, because AARP supports the President’s liberal causes.

As noted above, AARP executives e-mailed the White House in November 2009 stating that “the larger issue is how best to serve the cause.” It would thus appear that both AARP and the Administration recognize their political interests are aligned. Certainly the Administration’s actions – exemptions for Medigap coverage included both in statute and in rulemaking; attacks on insurers with smaller profit margins than AARP; failure to criticize AARP’s percentage-based compensation model – are consistent with a governing philosophy that permits AARP to engage in questionable and abusive behavior towards seniors, so long as AARP funnels the profits from said behavior back into supporting the Administration’s liberal causes.

In April 2010, Secretary Sebelius wrote to insurers to stop rescinding insurance policies earlier than required under the law, encouraging them “not to wait until the fall to do the right thing.”[79] America’s seniors have been waiting for years for Secretary Sebelius, and the entire Obama Administration, to do the right thing – to apply the law fairly, without regard to political persuasion. Unfortunately, the facts suggest that the Administration has knowingly looked the other way, and failed to take on AARP over its business practices – because political advantage outweighs the need for impartial enforcement, or extending the supposed benefits of the health care law to senior citizens.

Conclusion

Though it purports to be a seniors advocacy organization, AARP functions in many respects as an insurance conglomerate with a liberal lobbying arm on the side. Independent experts and even former AARP executives have admitted that the organization’s billions of dollars raised from its business enterprises – most notably the sale of health insurance plans – have compromised the organization’s mission and independence. As one consultant put it: “Either you’re a voice for the elderly or you’re an insurance company – choose one.”[80]

As this report has demonstrated, AARP has acted against its members’ interest, but in its own financial interests, on several occasions during the major health care debates of the past several years. First AARP endorsed a health care law that gave its most lucrative product offering – Medigap insurance – a major opportunity to solicit new members, exempted those Medigap plans from the law’s regulatory regime, and allowed AARP to continue imposing waiting periods on the sickest seniors looking to buy Medigap coverage. More recently, AARP has engaged in a covert lobbying campaign designed to kill Medigap reforms that would benefit nearly four in five policy-holders and improve Medicare’s solvency – but could cost AARP billions.

This year, AARP has embarked upon a “You’ve Earned a Say” campaign, purportedly designed to solicit members’ opinions on ways to reduce the deficit. However, the organization has yet to solicit members’ viewpoints about its own actions. For instance:

- How many members know that senior AARP executives have received over $1 million in compensation from the organization – and that 543 individuals received over $100,000 in compensation last year?

- How many members know that AARP has generated over $2 billion in revenue from selling health insurance plans in the past five years?

- How many members know that AARP imposes waiting periods on Medigap applicants with pre-existing conditions – and stood idly by as provisions to eliminate Medigap pre-existing condition discrimination were stricken from the health care law?

- How many members know that nearly four in five Medigap plan holders would financially benefit from reforms, to the tune of several hundred dollars per year?

- How many members know that Medigap reforms that would help seniors could cost AARP billions of dollars in lost revenue?

At the very least, AARP should be up-front and honest with its members about the massive financial stake it has in this debate. Better yet, the organization should start thinking less about its bottom line and more about its members, and endorse reforms that will help the vast majority of Medigap policy-holders.

[1]Behind the Veil: The AARP America Doesn’t Know, report by Reps. Wally Herger and Dave Reichert, March 29, 2011, http://herger.house.gov/images/stories/pdf/20110329aarpreport.pdf, p. 6.

[2]AARP Inc., 2010 Internal Revenue Service Form 990, http://www.aarp.org/content/dam/aarp/about_aarp/annual_reports/2010_990_aarp.pdf, p. 1.

[3] Ibid., pp. 8-9.

[4] AARP Inc., 2011 Consolidated Financial Statements, http://www.aarp.org/content/dam/aarp/about_aarp/annual_reports/2012-05/Consolidated-Financial-Statements-2011-2010-AARP.pdf, p. 3.

[5] Page 9 of the AARP 2011 financial statements notes that “the service provider United Healthcare Corporation accounted for 65% of total royalties earned in 2011 and 2010.” 65% of the total $704 million in royalties equates to $457.6 million received from United Healthcare.

[6] Ibid., p. 3.

[7] Letter from AARP Chief Operating Officer Thomas Nelson to Rep. Dave Reichert, November 2, 2009, pp. 3-4.

[8]AARP Inc., 2008 Consolidated Financial Statements, http://assets.aarp.org/www.aarp.org_/TopicAreas/annual_reports/assets/AARPConsolidatedFinancialStatements.pdf, pp. 4-9.

[9]Ibid., pp. 3-9.

[10]AARP Inc., 2009 Consolidated Financial Statements, http://assets.aarp.org/www.aarp.org_/cs/misc/2009_aarp_consolidated_financial_statements_12_31_09.pdf, pp. 3-9.

[11] AARP Inc., 2010 Consolidated Financial Statements, http://www.aarp.org/content/dam/aarp/about_aarp/annual_reports/2010_aarp_consolidated_financial_statements_12_31_10.pdf, pp. 3-9.

[12] AARP Inc., 2011 Consolidated Financial Statements.

[13] Fortune 500, Health Care: Insurance and Managed Care, May 23, 2011, http://money.cnn.com/magazines/fortune/fortune500/2011/industries/223/index.html.

[14] Ibid.

[15] Gary Cohn and Darrell Preston, “AARP’s Stealth Fees Often Sting Seniors With Costlier Insurance,” Bloomberg December 4, 2008, http://www.bloomberg.com/apps/news?pid=newsarchive&refer=&sid=a4OkPQIPF6Kg.

[16] Letter from Senate Finance Committee Ranking Member Chuck Grassley to AARP CEO William Novelli, November 3, 2008, http://www.grassley.senate.gov/news/upload/110320081.pdf.

[17] Robert Pear, “AARP Orders Investigation Concerning Its Marketing,” New York Times November 18, 2008, http://www.nytimes.com/2008/11/19/us/19insure.html?_r=1.

[18] Emily Berry, “United Stops Selling AARP Limited-Benefit Insurance,” Amednews.com May 28, 2009, http://www.ama-assn.org/amednews/2009/05/25/bisd0528.htm.

[19] Behind the Veil: The AARP America Doesn’t Know.

[20] Letter from House Ways and Means Committee Members Wally Herger, Charles Boustany, and Dave Reichert to Internal Revenue Service Commissioner Douglas Shulman, December 21, 2011, http://waysandmeans.house.gov/uploadedfiles/letter_to_irs-shulman_12-15-11.pdf.

[21] Congressional Budget Office, score of H.R. 6079, Repeal of Obamacare Act, July 24, 2012, http://cbo.gov/sites/default/files/cbofiles/attachments/43471-hr6079.pdf.

[22] Robert Book and Michael Ramlet, What Changes will Health Care Reform Bring to Medicare Advantage Plan Benefits and Enrollment?, Medical Industry Leadership Institute- Carlson School of Management, October 2011, http://americanactionforum.org/sites/default/files/Embargoed_Book+Ramlet_MILI-Working-Paper_2011-10-13_Final.pdf.

[23] Behind the Veil: The AARP America Doesn’t Know, Table 4, p. 16.

[24] The Moment of Truth, report of the National Commission on Fiscal Responsibility and Reform, December 2010,

[25] Restoring America’s Future, report of the Bipartisan Policy Center’s Debt Reduction Tax Force, November 2010, http://bipartisanpolicy.org/sites/default/files/BPC%20FINAL%20REPORT%20FOR%20PRINTER%2002%2028%2011.pdf, pp. 52-53.

[26] Overview of Coburn/Lieberman Medicare reform proposal, June 2011, http://www.coburn.senate.gov/public/index.cfm?a=Files.Serve&File_id=1ea8e116-6d15-46ba-b2e0-731258583305.

[27] White House Fiscal Year 2013 budget submission to Congress, February 2012, http://www.whitehouse.gov/sites/default/files/omb/budget/fy2013/assets/budget.pdf, p. 35.

[28] Kaiser Family Foundation, “Medigap Reforms: Potential Effects of Benefit Restrictions on Medicare Spending and Beneficiary Costs,” July 2011, http://www.kff.org/medicare/upload/8208.pdf, p. 8.

[29] Ibid.

[30] Ibid., Exhibit 2, p. 6.

[31] “AARP’s Stealth Fees Often Sting Seniors With Costlier Insurance.”

[32] Behind the Veil: The AARP America Doesn’t Know.

[33] Kaiser Family Foundation, “Potential Effects of Benefit Restrictions on Medicare Spending and Beneficiary Costs,” Exhibit 2, p. 6.

[34] Behind the Veil: The AARP America Doesn’t Know, Table 2, p. 9.

[35] AARP Inc., 2011 Consolidated Financial Statements, p. 3.

[36] AARP Press Release, “AARP to Super Committee: Don’t Cut Medicare, Social Security Benefits,” October 19, 2011, http://www.aarp.org/about-aarp/press-center/info-10-2011/aarp-to-super-committee-dont-cut-medicare-social-security-benefits.html.

[37] Carol Costello, “150,000 Seniors In Revolt,” CNN American Morning January 6, 2010, http://www.cnn.com/video/?/video/politics/2010/01/06/costello.aarp.health.care.cnn.

[38] AARP Press Release, “AARP Thanks Senate for Passing Health Care Reform,” December 24, 2009, http://www.aarp.org/about-aarp/press-center/info-03-2010/aarp_thanks_senateforpassinghealthcarereform.html.

[39] New York State Department of Financial Services, list of insurers offering Medicare supplemental coverage, http://www.dfs.ny.gov/insurance/caremain.htm#insurer.

[40] House Tri-Committee Health Reform Discussion Draft, June 19, 2009, http://democrats.energycommerce.house.gov/Press_111/20090619/healthcarereform_discussiondraft.pdf, p. 358.

[41] Susan Jaffe, “Medigap Supplemental Coverage Can Be Too Pricey for Younger Medicare Beneficiaries,” Kaiser Health News March 7, 2011, http://www.washingtonpost.com/wp-dyn/content/article/2011/03/07/AR2011030703978.html.

[42] Congressional Budget Office, preliminary estimate of House Tri-Committee Health Reform Discussion Draft, July 7, 2009, http://democrats.energycommerce.house.gov/Press_111/20090708/cbomedicare.pdf, p. 4.

[43] Letter from AARP Chief Operating Officer Thomas Nelson to Rep. Dave Reichert, November 2, 2009, p. 4.

[44] Karl Rove, “ObamaCare Rewards Friends, Punishes Enemies,” Wall Street Journal January 6, 2011, http://online.wsj.com/article/SB10001424052748704405704576063892468779556.html.

[45] House Energy and Commerce Subcommittee on Health hearing, “Prescription Drug Price Inflation: Are Prices Rising Too Fast?” December 8, 2009, http://energycommerce.house.gov/hearings/hearingdetail.aspx?NewsID=7588.

[46] AARP Press Release, “AARP Endorses Affordable Health Care for America Act,” November 5, 2009, http://www.aarp.org/about-aarp/press-center/info-11-2009/affordable_health_care_act_endorsement.html.

[47] Letter to the Editor, Wall Street Journal, by AARP President Lee Hammond, January 11, 2011, http://www.aarp.org/about-aarp/press-center/info-01-2011/aarp_letter_to_theeditor.html.

[48] House Energy and Commerce Committee, investigation into closed-door Obamacare negotiations, supplemental materials for June 8, 2012 memorandum, http://archives.republicans.energycommerce.house.gov/Media/file/PDFs/060812relevantdocsmemoIII.pdf, pp. 63-68.

[49] Ibid., p. 73.

[50] Ibid., p. 79.

[51] Ibid., p. 88.

[52] Jeffrey Young, “New AARP Chief Gave Big to Obama,” The Hill March 12, 2009, http://thehill.com/business-a-lobbying/3963-new-aarp-chief-gave-big-to-obama.

[53] Ibid.

[54] “AARP Leadership Profile: Nancy LeaMond,” http://www.aarp.org/about-aarp/executive-team/info-2009/Nancy_Leamond.html.

[55] “AARP Leadership Profile: Debra Whitman,” http://www.aarp.org/about-aarp/executive-team/debra_whitman/.

[56] “AARP Leadership Profile: Kevin Donnellan,” http://www.aarp.org/about-aarp/executive-team/info-2009/Kevin_Donnellan.html.

[57] “AARP Leadership Profile: Cindy Lewin,” http://www.aarp.org/about-aarp/executive-team/info-2010/cindy_lewin.html.

[58] Michael Muskal, “AARP Ads: Hands Off Social Security and Medicare,” Los Angeles Times September 21, 2011, http://www.standard.net/stories/2011/09/21/aarp-ads-hands-social-security-and-medicare.

[59] Gene Steuerle and Stephanie Rennane, “Social Security and Medicare Taxes and Benefits Over a Lifetime,” Tax Policy Center, June 2011, http://www.urban.org/UploadedPDF/social-security-medicare-benefits-over-lifetime.pdf.

[60] While the Associated Press story from December 30, 2010 has been removed from the AARP website, it can still be found at http://www.cbsnews.com/2100-204_162-7197847.html.

[61] Glenn Kessler, “AARP’s Misleading Ad about Balancing the Budget,” Washington Post June 20, 2011, http://www.washingtonpost.com/blogs/fact-checker/post/aarps-misleading-ad-about-balancing-the-budget/2011/06/17/AGQKRsYH_blog.html.

[62] AARP Press Release, “AARP Launches New TV Ad Calling on Congress to Protect Medicare and Social Security from Harmful Cuts,” June 16, 2011, http://www.aarp.org/about-aarp/press-center/info-06-2011/aarp-launches-new-tv-ad-calling-on-congress-to-protect-medicare-and-social-security-from-harmful-cuts.html.

[63] Section 9014 of the Patient Protection and Affordable Care Act (PPACA) as amended, http://housedocs.house.gov/energycommerce/ppacacon.pdf, pp. 816-18.

[64] AARP Inc., 2010 Internal Revenue Service Form 990, pp. 8-9.

[65] PPACA, Section 9010(h)(3)(C) as amended, p. 815.

[66] AARP Inc., 2011 Consolidated Financial Statements, p. 3.

[67] PPACA, Section 1001, p. 22.

[68] Section 1882(r)(1) of the Social Security Act, 42 U.S.C. 1395ss(r)(1).

[69] Department of Health and Human Services, Rate Increase Disclosure and Review, Final Rule, Federal Register May 23, 2011, http://www.gpo.gov/fdsys/pkg/FR-2011-05-23/pdf/2011-12631.pdf, pp. 29966-67, 29985.

[70] Department of Health and Human Services, Rate Increase Disclosure and Review, Proposed Rule, Federal Register 23 December 2010, http://www.gpo.gov/fdsys/pkg/FR-2010-12-23/pdf/2010-32143.pdf, pp. 81007, 81009, 81026.

[71] Official HHS Biography of Secretary Kathleen Sebelius, http://www.hhs.gov/secretary/about/biography/index.html.

[72] Remarks by HHS Secretary Kathleen Sebelius at the Democratic National Convention, September 4, 2012, http://dyn.politico.com/printstory.cfm?uuid=CB187143-9624-3760-BC9CC2DBE9C60BD7.

[73] Remarks by the President at the Democratic National Convention, September 6, 2012, http://www.whitehouse.gov/the-press-office/2012/09/07/remarks-president-democratic-national-convention.

[74] Jane Norman, “Sebelius Urges Health Care Insurers to Trim Their Profits,” CQ HealthBeat March 10, 2010, http://www.commonwealthfund.org/Newsletters/Washington-Health-Policy-in-Review/2010/Mar/March-15-2010/Sebelius-Urges-Health-Insurers-to-Trim-Their-Profits.aspx.

[75] “Top Industries: Most Profitable,” 2009 Fortune 500, http://money.cnn.com/magazines/fortune/fortune500/2009/performers/industries/profits/.

[76] HHS Press Release, “HHS Secretary Kathleen Sebelius Urges Wellpoint to Immediately Stop Dropping Coverage for Women with Breast Cancer,” April 23, 2010, http://www.hhs.gov/news/press/2010pres/04/20100423a.html.

[77] Remarks of HHS Secretary Kathleen Sebelius at AARP Orlando@50+ Conference, October 1, 2010, http://www.hhs.gov/secretary/about/speeches/sp20101001.html.

[78] Office of Special Counsel, File No. HA-12-1989 (Kathleen G. Sebelius), September 12, 2012, http://www.osc.gov/documents/hatchact/Hatch%20Act%20Report%20on%20HHS%20Secretary%20Kathleen%20Sebelius.pdf.

[79] HHS News Release, “Momentum Building on Sebelius’ Challenge to Insurers to Ban Rescission Before Law Takes Effect in September,” April 28, 2010, http://www.hhs.gov/news/press/2010pres/04/20100428a.html.

[80] Cited in Dan Eggen, “AARP: Reform Advocate and Insurance Salesman,” Washington Post October 27, 2009, http://www.washingtonpost.com/wp-dyn/content/article/2009/10/26/AR2009102603392_pf.html.